Why Digital Risk Processing is Becoming the New Operating Model for Commercial Insurance

Blogs

Commercial insurance has long operated on a paradox. While every commercial insurance policy begins with a submission, for most insurers, the submission intake process remains one of the most fragmented and manual parts of the insurance value chain.

Submissions arrive through multiple channels, often containing emails, PDFs, spreadsheets, applications, loss runs, and supporting documents. Before underwriting can begin, teams must review, classify, route, validate, and organize information scattered across these documents. As a result, underwriters spend up to 70% of their time on non-underwriting activities, with roughly 40% devoted to administrative tasks such as data extraction and processing.

Delays, incomplete information, and inconsistent routing do not end there and create downstream bottlenecks across risk assessment, servicing, distribution, and portfolio management.

To address these challenges, insurers are increasingly adopting Digital Risk Processing (DRP), an operating model that transforms incoming submission data into structured, decision-ready risk intelligence.

Submission intake: The first bottleneck in commercial insurance

Commercial insurance information rarely arrives in a standardized format. A single submission may contain dozens of documents, attachments, forms, emails, and supporting materials. Critical details are often buried within unstructured text, making extraction and analysis both time-consuming and error-prone.

But the challenge extends beyond data capture. Before underwriting, claims, servicing, or distribution teams can act, submissions must first be reviewed, classified, and routed to the appropriate business unit.

In many organizations, this process remains highly manual. Operations teams often determine where a submission should go based on factors such as line of business, geography, broker relationships, risk appetite, and workload availability. When information is incomplete or routing decisions are inconsistent, submissions can sit in queues, be reassigned multiple times, or require additional follow-up before work can begin.

This creates several operational challenges:

- Longer processing and response times

- Increased workload for operations teams

- Delays caused by manual triage and routing

- Higher operational costs

- Reduced visibility across business functions

- Missed growth opportunities due to capacity constraints

The challenge becomes even more significant in specialty and middle-market insurance, where submissions can be highly complex and require extensive review before reaching the right teams.

As submission volumes continue to rise, insurers are discovering that simply adding more staff is not a sustainable solution. Improving submission intake and routing has become a critical first step toward improving performance across the entire insurance lifecycle.

Why submission intake needs a new operating model

Digital Risk Processing represents a fundamental shift from document-centric insurance workflows to data-centric operations.

Rather than treating submissions as collections of files, DRP treats them as sources of structured risk intelligence. Advanced technologies, including artificial intelligence, machine learning, natural language processing, and Insurance Process Automation, extract relevant information, validate it, enrich it with internal and external data sources, and present it in a format that supports decisions.

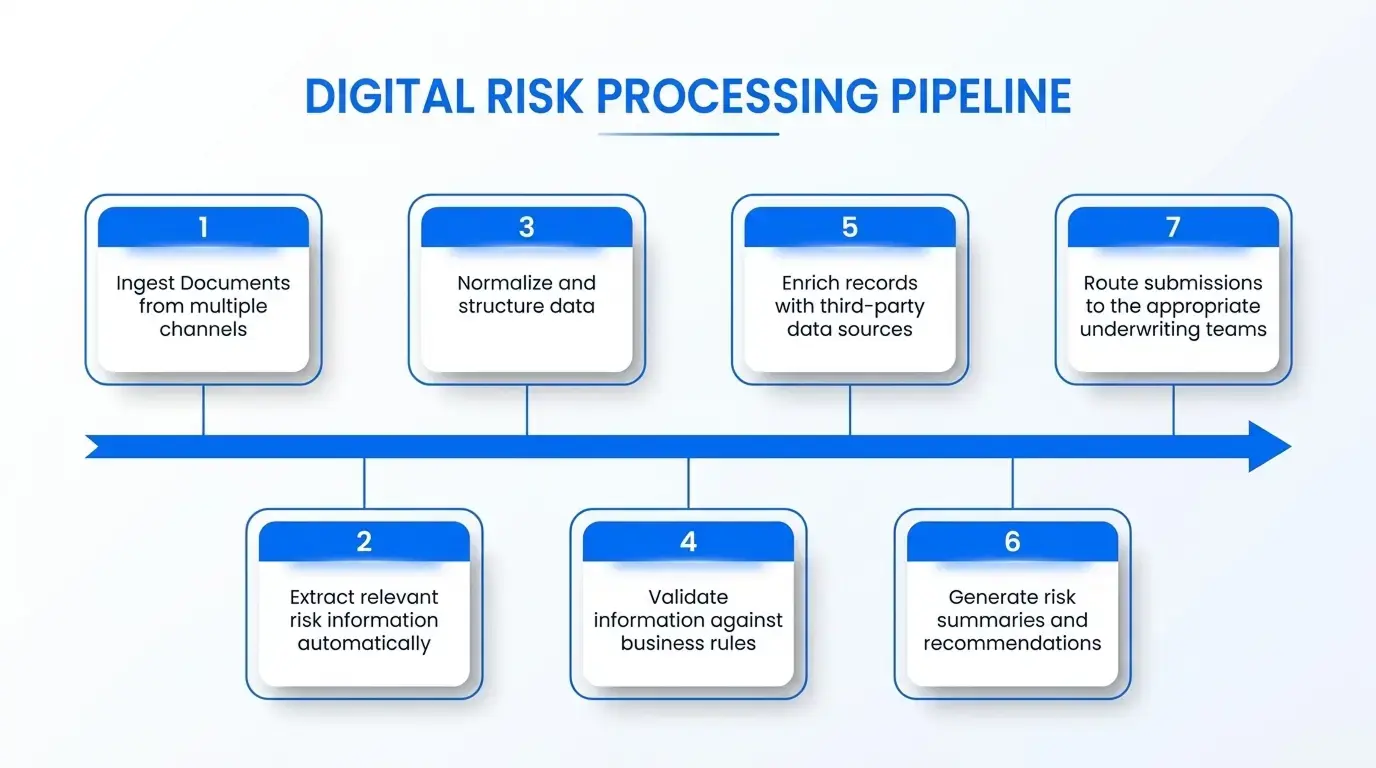

The objective is not to replace human resources. Instead, it is to eliminate low-value administrative work and allow teams to focus on evaluating risk, pricing, portfolio strategy, and more effective risk handling. In a DRP model, submissions move through a digital pipeline that can:

The result is a more efficient and scalable workflow powered by intelligent insurance automation.

Why insurers are modernizing submission intake

Several market forces are accelerating investment in modern intake capabilities.

1. Speed has become a competitive advantage

Brokers, policyholders, and distribution partners increasingly expect faster responses and seamless experiences.

Whether the interaction involves a new business submission, policy servicing request, endorsement, renewal, or claim, delays during intake create friction and negatively impact customer experience.

By automating intake and triage processes, insurers can significantly reduce cycle times while improving responsiveness across the organization.

The endorsement process is perhaps the most glaring gap. A broker needs to add a new employee or upgrade a plan. In practice, at many insurers, this means an email, a manual process, and a wait that can stretch days.

2. Operational capacity is under pressure

Many insurers face growing workloads while simultaneously managing talent shortages and workforce transitions.

As experienced insurance professionals retire and submission volumes continue to increase, organizations must find ways to scale operations without proportionally increasing headcount.

Modern intake capabilities help organizations maximize employee productivity by reducing repetitive administrative work and enabling teams to focus on higher-value activities.

3. Data quality directly impacts business performance

Incomplete, inconsistent, or inaccurate information can create challenges throughout the insurance lifecycle.

Poor data quality affects decision-making, customer service, operational efficiency, reporting, compliance, and analytics.

By extracting, validating, and standardizing information at the point of intake, insurers can improve downstream processes and create a stronger foundation for enterprise-wide decision-making.

4. Enterprise visibility requires structured data

Many insurers still operate with critical information trapped in emails, PDFs, spreadsheets, and disconnected systems.

Without structured intake data, it becomes difficult to gain visibility into workload volumes, operational performance, customer interactions, risk concentrations, and business trends.

Modern intake frameworks convert incoming information into searchable, reusable data that supports analytics, reporting, and operational transparency across the enterprise.

Beyond data capture: Turning intake data into risk intelligence

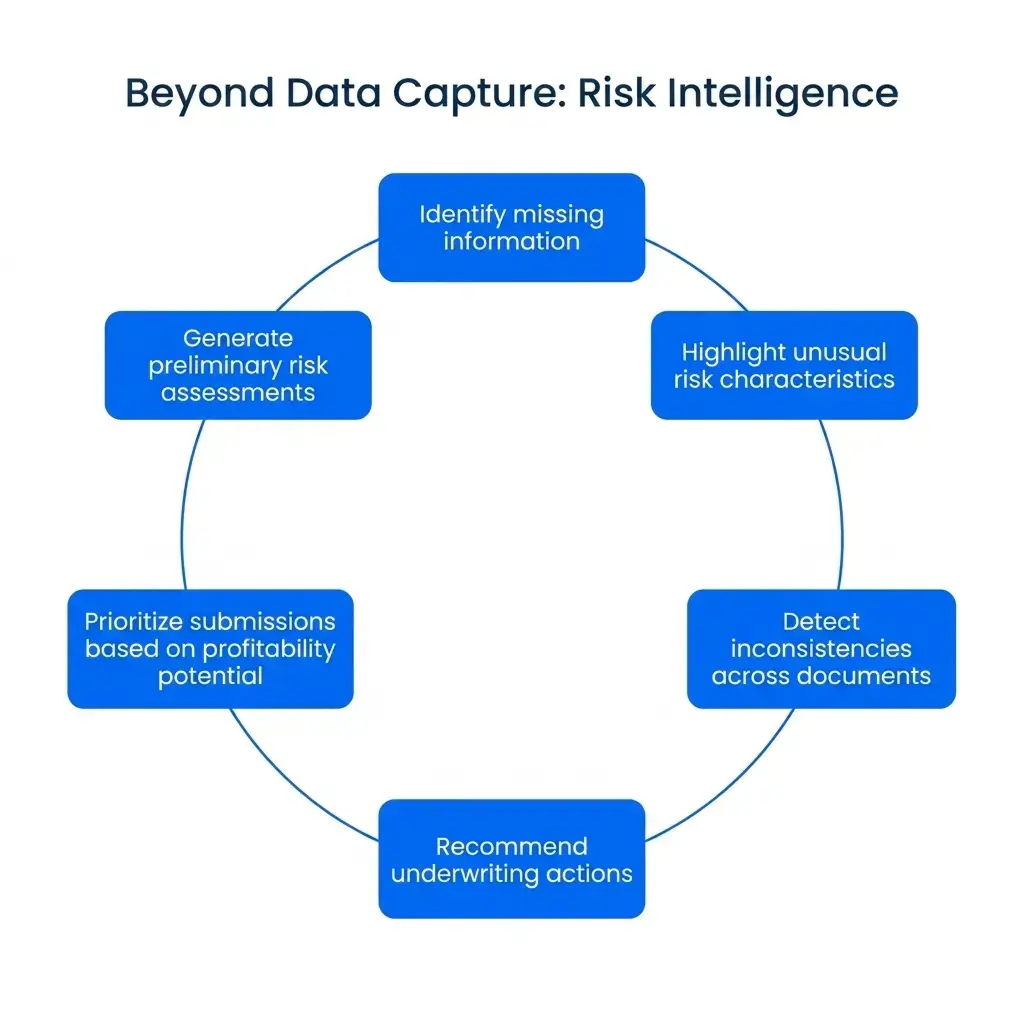

The most advanced Digital Risk Processing initiatives go beyond document automation. Leading insurers are beginning to use AI-driven models that can:

This progression transforms insurance operations from reactive document processing into proactive decision intelligence. Instead of searching through files for relevant details, teams receive structured information and actionable insights that support more consistent decisions across the enterprise.

AI-powered agents are increasingly helping insurers automate parts of this journey by identifying missing information, validating submissions, recommending next actions, and supporting teams with contextual guidance throughout the intake-to-decision process.

Creating better starting points across the insurance lifecycle

One common misconception is that intake modernization only benefits underwriting.

In reality, intelligent submission intake creates value across the entire insurance lifecycle:

Underwriting gains cleaner, structured information for risk evaluation.

Claims receives organized documentation and faster case setup.

Distribution teams gain improved visibility into pipeline activity and broker interactions.

Customer servicing teams can process requests more efficiently and consistently.

Operations leaders gain greater visibility into workloads, performance, and resource allocation.

The value comes from creating a better starting point for every downstream process that depends on accurate information.

Building an intelligent submission intake framework

Successful implementation of DRP requires more than technology deployment. Insurers must rethink workflows, governance, and organizational processes.

Key elements include:

- Centralized submission intake

- AI-powered document processing

- Data quality and governance frameworks

- Integration with core underwriting systems

- Human-in-the-loop review processes

- Continuous model monitoring and improvement

Organizations that treat DRP as an enterprise operating model rather than a standalone automation project tend to achieve the greatest value. This approach aligns closely with broader insurance workflow automation programs aimed at improving operational agility, consistency, and scalability.

Many insurers are also adopting centralized insurance underwriting workbench capabilities to provide their teams with a unified view of submission data, risk insights, and decision-support tools.

Connecting submission intake to better insurance outcomes

Commercial insurance is entering a period where operational performance will increasingly depend on how effectively organizations capture, process, and act on incoming information.

Digital Risk Processing is emerging as the operating model that makes this possible. By combining AI, automation, workflow orchestration, and data intelligence, DRP enables insurers to modernize submission intake, improve data quality, accelerate decision-making, and create a stronger foundation for downstream processes across the insurance value chain.

However, achieving these outcomes requires more than standalone automation tools. Insurers need a connected platform that can orchestrate the entire Digital Risk Processing journey.

Neutrinos helps insurers transform submission intake into a structured, intelligence-driven workflow by connecting each stage of the process—from submission capture and document ingestion, to data extraction, validation, risk intelligence generation, and decision support.

We bring together AI-powered document processing, workflow orchestration, intelligent agents, and enterprise integrations, enabling insurers to move from fragmented intake operations to a unified intake-to-decision model.

The result is faster submission handling, higher-quality data, more informed underwriting decisions, and better outcomes across servicing, claims, distribution, and other downstream functions. Want to experience these advantages too? Connect with our experts now to get started.